The post ACPL’s Sidharth Gupta on Taking Manufacturing Muscle to End Consumers with TrueSilver appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>This strategic shift marks ACPL’s transition from being a behind-the-scenes global manufacturer to building a strong, consumer-driven presence in India’s fast-evolving silver jewellery market. Leveraging its export-grade craftsmanship, large-scale manufacturing capabilities, and stringent quality certifications, the company is now bringing the same global standards directly to Indian buyers through a digital-first retail approach.

In this conversation with Solitaire International, Gupta reflects on ACPL’s journey and evolution in the international silver jewellery landscape, the business rationale behind entering the D2C space, key trends shaping domestic demand, and how the company’s export legacy is being translated into a differentiated retail proposition. He also outlines the long-term vision for TrueSilver as a significant growth driver within ACPL Exports’ broader strategy.

ACPL has built a solid reputation as a global manufacturing powerhouse. What consumer insights convinced you to enter the Indian D2C silver jewellery space with TrueSilver?

ACPL has been manufacturing sterling silver jewellery for over five decades and exporting globally for nearly 40 years, with strong exposure to markets such as the United States. Through this journey, we developed a deep understanding of silver jewellery trends and quality benchmarks worldwide.

In India, however, the silver jewellery market has largely remained unorganised and cottage industry driven. With rising brand awareness, aspirational buying behaviour and changing consumer preferences, we felt the category was ready to redefine itself.

We are seeing millennials and younger audiences increasingly gravitate towards silver as a preferred, contemporary option to accessorise for different occasions. These shifts collectively convinced us that it was the right time to build a consumer-facing brand in India.

You are deeply aligned with technology and digital systems. How are you leveraging AI, data analytics, or consumer behaviour tracking to shape product design, pricing, and inventory planning for TrueSilver?

At this stage, our digital focus is centered on building awareness and reaching digitally savvy consumers efficiently. We began as a pure play D2C brand because our target audience is highly active online, and digital allows better cost efficiencies in customer acquisition.

Operationally, our strength lies in being a vertically integrated manufacturing company. This gives us tighter control over production, inventory, and pricing compared to brands that source externally. Additionally, having supplied to a large number of retailers across India in our B2B business, we have strong market mapping and category insights, which help us plan inventory with precision.

With nearly 900 SKUs at launch, will the brand employ digital tools to manage assortment planning and ensure trend responsiveness, especially for today’s consumers?

We have launched approximately 700 to 800 SKUs across categories including earrings, rings, bracelets, necklaces, anklets and toe rings. Our approach is guided by long-standing category expertise and consumer understanding built over decades.

Being vertically integrated allows us flexibility in manufacturing and faster response to demand trends. Since we control production, we can manage assortment depth and replenishment efficiently as we scale across digital and offline channels.

Tell us more about customising jewellery. Will it be a challenge to cater to such demand?

Personalisation is a huge trend in the US and Europe, and we have the largest range of personalized jewellery ranging from rings, bracelets, etc. We have about 100+ styles available on the website. Given our own strengths in manufacturing, the turnaround time for creating these pieces is faster. Styles that include initials, birthstone preferences, photographs, thumb prints, etc., are most sought after for gifting or personal purchases.

You’ve set a revenue target of ₹100 crore, scaling to ₹250 crore with 100 retail stores. How will the brand balance the evolution between your own D2C platform, marketplaces, and offline retail channels?

We have adopted a phased approach. Currently, we are digital-first, operating through our own website and key marketplaces such as Amazon and Myntra, with plans to expand across other leading platforms.

In the second phase, we plan to launch company-owned stores in metros including Delhi, Mumbai and Bengaluru.

Will TrueSilver be sold only in India or would you expand to foreign markets as well since your parent company has a strong export network across the globe?

International expansion is part of our roadmap. ACPL already works with retailers globally and has deep market understanding in the US, Europe and other regions.

For TrueSilver, we intend to begin with a digital rollout in the US, UK, and UAE markets, leveraging online channels and fulfilment partnerships. Physical retail in select international markets is under evaluation and will be considered at a later stage.

Looking ahead, do you see TrueSilver evolving into a tech-enabled omnichannel brand — perhaps integrating virtual try-ons, AR-led shopping, or blockchain-backed purity verification?

Our immediate focus is on building strong digital awareness through D2C, marketplaces and physical retail. As we scale, we remain open to integrating advanced digital tools that enhance customer confidence and experience.

Quality assurance remains central to our positioning, and as a long-standing sterling silver manufacturer adhering to global standards, we are fully compliant with BIS hallmarking norms.

Silver in India has often been perceived as either occasion-led or price-driven. How are you proposing to reposition silver as an everyday lifestyle choice for younger consumers?

We are positioning sterling silver as modern, lightweight, and wearable for everyday use. Globally, sterling silver is widely accepted as a fashion-forward yet precious category. In India, it has traditionally been either occasion focused or unbranded.

With gold becoming significantly more expensive, consumers are looking for accessible alternatives that still offer intrinsic value. We see younger audiences adopting silver as part of everyday styling rather than waiting for special occasions. TrueSilver aims to formalise and premiumise the category through assured purity and contemporary designs.

With decades of manufacturing legacy behind ACPL, what internal cultural or operational shifts were necessary to transition from a pure B2B exporter to building a consumer-facing brand?

As a B2B exporter, our focus was largely on global standards manufacturing and retailer partnerships. Moving into a D2C model required us to build marketing, digital outreach and direct consumer engagement capabilities.

However, our strong foundation in manufacturing, category insights and retail mapping has enabled a smoother transition. Being vertically integrated allows us to control the full value chain — from product designs to production and customer delivery — which is a significant structural advantage in building a consumer brand. We are also focused on customer insights, leveraging them to our designs and brand building.

Marketplace platforms such as Amazon India and Myntra are highly competitive. What will differentiate TrueSilver in such crowded digital environments?

Our differentiation lies in assured sterling silver purity, manufacturing credibility and breadth of assortment. We offer over 900 SKUs across categories with accessible entry pricing starting at ₹1,000.

As one of the largest exporters in this category, our legacy and quality standards provide trust, while our vertically integrated structure supports competitive pricing and healthier margins compared to pure trading brands.

How do you plan to navigate silver price volatility while maintaining accessible pricing and healthy margins in the domestic market?

Silver prices, like all precious metals, are subject to volatility. However, our vertically integrated model offers greater control over cost structures. Since we manufacture in-house rather than sourcing finished goods, we have operational flexibility.

While short-term fluctuations can create instability, we are also seeing increased consumer interest in silver. Our focus remains on offering value-driven price points while managing margins through operational efficiencies.

Over time, ACPL expects its branded portfolio to contribute 30–40% of overall revenue. How will you ensure that the D2C business strengthens your established global B2B partnerships?

Our B2B export business and our D2C brand operate with distinct market strategies. The experience and global standards developed through decades of export partnerships form the backbone of TrueSilver’s credibility.

Rather than competing, the two segments complement each other. Our global exposure strengthens product understanding and quality benchmarks, while the branded play enables us to participate directly in evolving consumer trends in India.

The post ACPL’s Sidharth Gupta on Taking Manufacturing Muscle to End Consumers with TrueSilver appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The post IJEX 6TH Fam Maps UAE Market Opportunities for Indian Exporters appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The 6th batch of the IJEX FAM Programme, initiated and facilitated under GJEPC’s Export Mentorship Programme (EMP), delivered a structured five-day immersion into the UAE jewellery ecosystem, combining market intelligence, design orientation, logistics guidance, and extensive retail visits across Dubai, Abu Dhabi, and Sharjah. Participants consistently highlighted the programme’s practical value, mentorship, and clarity in building export readiness.

Day 1: Understanding the Middle East Landscape

The programme commenced at IJEX with an introduction session followed by a presentation on navigating the Middle East jewellery market, covering regional dynamics, consumer preferences across emirates, export opportunities, and positioning strategies across wholesale and retail segments. Delegates then visited Ithraa Wholesale & Retail, Goldcenter Building, Gold House, Jewel Plaza, Traditional Gold Souq, African Souq, and Gold Land, together representing around 475 retailers and 460 offices, giving participants a broad view of both wholesale and traditional trading ecosystems.

Akshit Dhameliya, Grown Carbon, noted that the programme helped convert his export vision into practical reality, describing IJEX as a strong foundation for his goal of becoming an exporter.

Day 2: New Dubai Retail and Design Insights

A designer interaction session focused on branding, cultural motifs, and regional aesthetics relevant to GCC consumers. Market visits to Mall of the Emirates, Lulu Hypermarket – Al Barsha, Gold & Diamond Park, and Dubai Hills Mall allowed delegates to observe nearly 115 jewellery retailers across luxury malls, diaspora-focused outlets, and specialised diamond boutiques, highlighting differences in merchandising, product mix, and customer behaviour.

Dhaval Patel, Myora Fine Jewellery, highlighted that the programme provided valuable understanding of jewellery requirements across different markets and locations, strengthening his insight into the global jewellery ecosystem.

Day 3: Logistics, Compliance and Market Diversity

A session by Ferrari Freight Forwarders covered import procedures, documentation, duties, and secure logistics handling. Subsequent visits to Dubai Mall, Dubai Design District (d3), Karama Centre, and Meena Bazaar brought delegates in contact with about 150 retailers, spanning ultra-luxury international brands to culturally driven Indian diaspora markets, reinforcing the diversity of customer segments within the UAE.

Madhukar Ranka, Vardhman Jewels Tech Pvt. Ltd., Mumbai, described the programme as enriching and well-structured, noting that the combination of sessions and market visits created strong learning even for participants aspiring to enter international markets.

Day 4: Abu Dhabi Market Exploration

Visits to Madinat Zayed Gold Centre, Hamdan Street, and Abu Dhabi Mall covered roughly 132 jewellery stores, offering insights into the capital’s consumer preferences across luxury, traditional Arabic styles, and price-sensitive segments. Delegates reported improved clarity in identifying suitable positioning and product strategies for different emirates.

Kumarpal Jain, SSP Jewels Pvt. Ltd., emphasised that the team’s continuous support and responsiveness helped participants understand retailer networks and market opportunities, adding that he would consider establishing an office presence after gaining more experience in the region.

Day 5: Strategy Alignment and Expansion

The final day focused on one-to-one consultations with the IJEX team, followed by a certificate ceremony and a visit to Sharjah Blue Souq, where delegates explored around 110 jewellery stores known for 18kt, 21kt, and 22kt gold, diamonds, and silver collections, further expanding their understanding of regional demand across the Northern Emirates.

Priyanka Jalan, Ouro Jewels, stated that the programme was thoughtfully planned and provided a clear understanding of the ecosystem while creating meaningful opportunities, appreciating the leadership and support extended by the IJEX team throughout the experience.

Overall, participants described the programme as informative, well-organised, and strongly supportive, with several stating that the experience provided clarity, confidence, and a concrete roadmap for entering export markets through IJEX.

The post IJEX 6TH Fam Maps UAE Market Opportunities for Indian Exporters appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The post Broken Supply Chains: Why Retail Growth Isn’t Lifting Diamonds appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The traditional model that shaped demand across the diamond distribution chain has been fundamentally disrupted.

In the past, strong retail performance created a ripple effect throughout the pipeline. As sales rose, jewellers placed larger orders, lifting polished demand, and manufacturers responded by buying more rough to meet those needs.

The impact was exponential. A modest increase in retail sales translated into a sharper rise in polished demand and an even stronger boost in the rough market, as Pranay Narvekar, partner at Pharos Beam Consultancy, describes in what he calls the bullwhip effect.

That dynamic was most visible in the first quarter, when polished and rough trading typically spiked as jewellers replenished inventory sold during the holiday season.

The cycle is still there, but it is playing out at lower levels, even as retail jewellers continue to report steady sales growth.

In the luxury segment, Richemont reported a 6% year-on-year increase in revenue from its jewellery maisons in the fourth quarter. Kering’s jewellery houses posted an estimated 9% improvement in the same period, while LVMH’s watch and jewellery division edged up 1%.

Among more commercial players, Signet Jewelers and Brilliant Earth are due to report in March, but Birks Group already noted a 12% rise in holiday sales. In the US independent channel, data provider Tenoris estimates overall jewellery sales among speciality jewellers grew 5.6% in 2025.

The positive trend extended internationally. Hong Kong-based Chow Tai Fook reported an 18% increase in sales and Luk Fook posted 26% growth during the October to December period. In India, Titan Company’s jewellery income rose 24% for the quarter, while Australia-based Michael Hill said sales increased 3% in the second half of calendar 2025.

These companies do not represent the entire retail landscape, but they do have a growing market share and benefit from significant marketing muscle. Their results point to a clear improvement in jewellery retail, and it has been some time since growth was this broad based across so many major players.

Why has that not translated into stronger polished and rough sales?

The answer is that while overall jewellery revenue has risen, retail sales of natural diamonds have declined.

Diamonds, both natural and lab-grown, now account for roughly 41% of total jewellery sales, down from about 50% a decade ago, according to Sherry Smith, partner at the Retail Smiths, a jewellery industry advisory, in a recent podcast with National Jeweler.

Several factors contributed to the decline.

First is the steady gain in market share by lab grown diamonds, particularly in bridal. Among more than 10,000 US couples surveyed who married in 2025, 61% chose a lab-grown diamond for their engagement ring, according to The Knot’s Real Weddings Study. As more retail jewellers actively present lab-grown alongside natural, and often lead with it, a growing share of diamond unit sales is shifting away from natural goods.

Second is the resulting issue of segmentation. Lab-grown stones typically sell at a significant discount to natural equivalents. Retailers are presenting both options to align with different consumer budgets, but that has squeezed the 0.50-carat to 1.50-carat natural centre stone segment, as customers opt for larger lab-grown pieces at similar price points.

That shift has made retailers more selective in the natural diamonds they purchase. Demand has gravitated toward larger, higher value stones, narrowing the range of goods that move consistently through the pipeline and leaving mid-size categories under pressure.

Third is the effect of higher gold prices. Gold jewellery was a major driver of overall sales growth last year, particularly among Hong Kong, China and India-based jewellers. As gold has surged, it has absorbed a greater portion of the consumer’s budget within a finished piece. To maintain price points, manufacturers are adjusting designs, often reducing diamond content or using smaller accent stones. The result is fewer natural diamonds embedded in each item sold, even when overall jewellery revenue appears stable or growing.

Another factor is consolidation at retail. There are simply fewer jewellers operating today than there were a decade ago, with the number of jewellery businesses operating in the US declining by about 2% to 3% per year, according to the Jewelers Board of Trade (JBT). Even if the surviving retailers are stronger and more efficient, fewer doors naturally translate into fewer diamond orders.

At the same time, those jewellers are running leaner inventories. The lessons of the pandemic, tighter credit conditions and volatile pricing have pushed retailers to manage stock more cautiously. They are replenishing faster and buying closer to confirmed demand rather than building inventory to hold.

Taken together, these trends explain the disconnect between healthy jewellery sales and weak diamond demand upstream. The industry is not necessarily selling fewer pieces of jewellery, but it is selling fewer natural diamonds per piece, through a smaller and more cautious retail base.

The traditional multiplier effect that once lifted polished and rough when retail performed well has weakened. Growth at the counter no longer guarantees momentum in the midstream or at the mines. Until natural diamonds regain share, value and volume at the retail level, the rest of the diamond supply chain will continue to realign at lower levels. Top of Form

The post Broken Supply Chains: Why Retail Growth Isn’t Lifting Diamonds appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The post GJEPC’s 4th Export Mentorship Program Prepares New Entrants for Global Markets appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

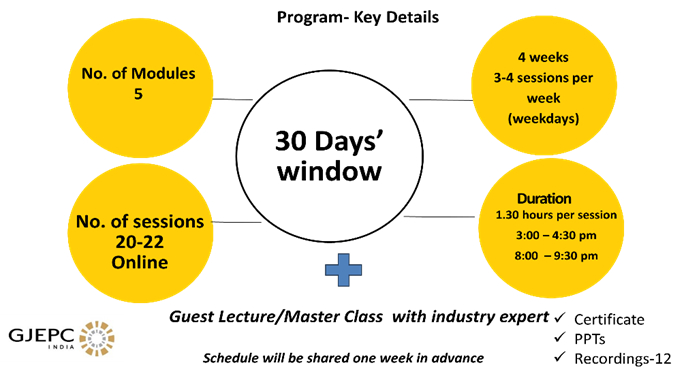

]]>The Gem & Jewellery Export Promotion Council (GJEPC) commenced the 4th batch of its Export Mentorship Program (EMP) with an orientation session on 19 January 2026, bringing together more than 85 participants for a one-month structured initiative aimed at converting industry members into export-ready enterprises. The programme, comprising 22 sessions, focuses on practical mentoring, policy awareness, and market alignment to strengthen India’s gems and jewellery export ecosystem.

The Orientation session featured a detailed presentation of the programme’s vision and framework by Sabyasachi Ray, Executive Director, GJEPC, who outlined the need to build a new generation of exporters from within the sector while bridging the gap between policy support mechanisms and industry-level export readiness. Participants were provided clarity on the programme structure, expected outcomes, and the conversion-focused approach adopted by the Council.

From Awareness to Exports

The EMP initiative is designed to move participants beyond theoretical understanding toward actual export conversion, aligned with India’s national objective of achieving $2 trillion in exports by 2030. The programme aims to build product readiness, market readiness, compliance awareness, and confidence among participants to enter international markets. It also reflects the Council’s role in connecting industry stakeholders with government policies, trade opportunities, and global buyer platforms.

Program Structure and Training Framework

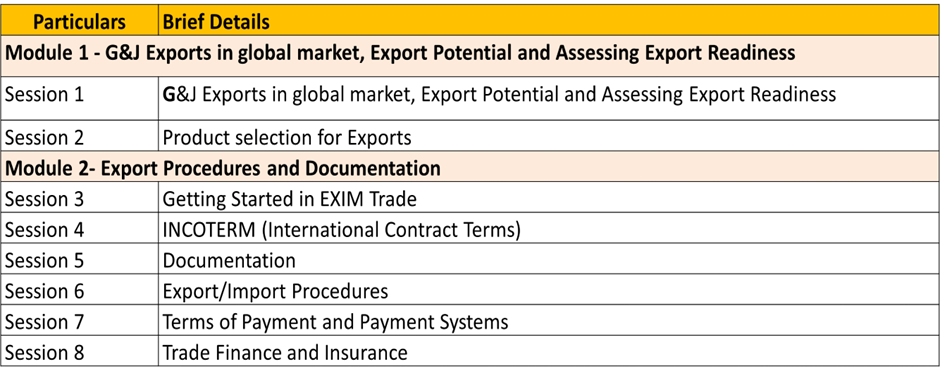

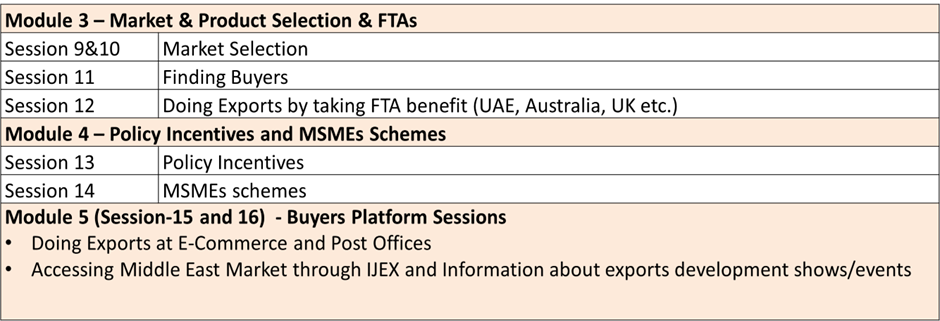

The EMP-4 program has been structured into multiple modules including product and market selection, export procedures and documentation, payment systems, trade finance, Free Trade Agreements (FTAs), policy incentives, digital platforms, and buyer-connecting mechanisms.

The program follows a phased approach beginning with knowledge sessions and progressing toward practical application and handholding for onboarding support for export platforms. Participants are guided through real-time exercises, documentation practices, and market analysis tools to ensure that the learning translates into actionable export strategies.

Details of the One–Month Exporter Mentorship Program

Product Identification and Market Selection

Product Identification and Market Selection

- Identification of export-ready products through structured HSN code mapping and product positioning.

- Access to global demand and import trend data to evaluate real market potential.

- Hands-on training on using international trade databases for product and market analysis.

- Framework to assess competition, pricing, and comparative advantage before selecting export products.

- Guidance on selecting the right product–market combination based on duties, logistics cost, and certification requirements.

- Practical exercises to shortlist target markets and viable product categories for each participant.

Compliance, Documentation, and Finance Training

The program provided detailed training on export procedures, documentation, and financial compliance. Participants were introduced to export documentation cycles, GST processes, shipping procedures, and payment security mechanisms. Sessions covered invoices, packing lists, certificates of origin, shipping bills, and banking procedures. Training on payment terms, letters of credit, escrow systems, and export finance ensured that participants understand risk mitigation and secure transaction practices. Government schemes, policy incentives, and MSME support frameworks were also explained to help exporters utilise available benefits effectively.

FTAs, and Reaching to Indian Diaspora as Market Entry Strategy

The program also included sessions on leveraging Free Trade Agreements, digital marketplaces, and buyer-connecting platforms. Participants were trained to understand tariff advantages, rules of origin, and pricing competitiveness in FTA markets. Digital export channels, e-commerce platforms, and diaspora-based market entry strategies were discussed to help participants access global buyers. The structured training approach ensures that participants are equipped not only with knowledge but also with pathways to connect with international markets and convert learning into export transactions.

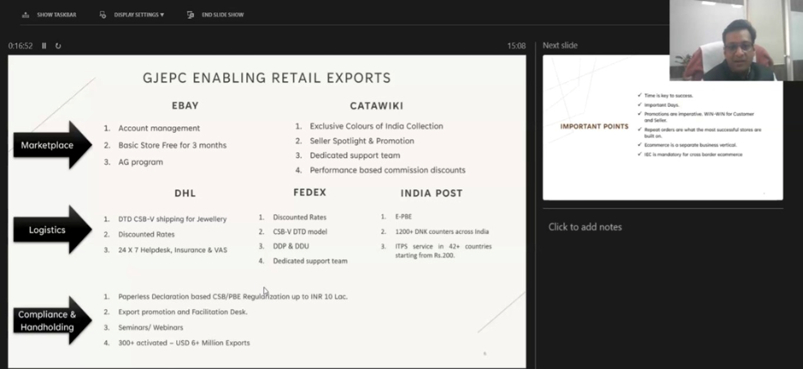

Buyer Connecting Platforms- E-Commerce, IJEX, Trade Shows/BSMs

A focused module on Buyer Connecting Platforms was delivered to provide participants with structured access to international markets through both institutional and digital channels. The sessions covered engagement through IJEX – India Jewellery Exposition Centre, Dubai, highlighting its role in facilitating Middle East market access, buyer-seller meetings, and re-export opportunities. In addition, dedicated sessions on cross-border e-commerce exports guided participants on cargo classification, documentation requirements, AD code registration, shipping procedures, and onboarding on digital platforms. Practical insights were provided on selecting the appropriate channel based on product type, shipment value, compliance norms, and target market dynamics, enabling participants to move from theoretical learning to actionable buyer connection strategies.

Way Forward

Through its structured sessions and mentoring approach, the EMP-4 program is enabling participants to transition from domestic business operations to export-oriented enterprises. The training provides clarity on product selection, market entry, compliance requirements, and financial planning, thereby strengthening export readiness across participating units.

By supporting 85+ participants through a one-month intensive program, the initiative contributes to building a stronger exporter base within the gems and jewellery sector and supports the broader national objective of expanding India’s global trade presence.

The post GJEPC’s 4th Export Mentorship Program Prepares New Entrants for Global Markets appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The post VAIRAM 2026 Looks Beyond Gems, Spotlights LGDs’ High Value Deep-Tech Applications appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The dignitaries present at the opening ceremony were Prof. Manu Santhanam, Dean (IC&SR), IIT Madras; Sanket Patel, Convener – LGD Committee, GJEPC; M.S. Ramachandra Rao, Head of the India Centre for Lab Grown Diamond (InCent-LGD) at IIT Madras; Jayanti Savaliya – Gujarat Region Chairperson, GJEPC; Ashish Borda, Convener – PMBD, GJEPC; Mital Doshi, Convener, BITC, GJEPC; and Sabyasachi Ray, Executive Director, GJEPC. Also present on the occasion were Manish Jiwani, Co-Convener, LGD Panel, GJEPC and Bharat Ghori, Co-Convener – MSME, GJEPC.

Addressing the gathering, Sabyasachi Ray, Executive Director, GJEPC, said, “As a Council, we have always tried to remain at the forefront of where the diamond and jewellery industry is heading. What we realised over time was that while India had manufacturing strength, the research component was missing. That understanding led to discussions with the Government and eventually to the creation of this InCent-LGD centre with strong support. Today, GJEPC’s role is to act as an interface between the trade and the technology ecosystem, so that the industry can benefit from the innovations being developed here and use this platform to expand into new opportunities.”

The day’s sessions focused on topics such as Research to Commercialisation, HPHT Technology Scale-Up, Advanced Applications Beyond Gems, and Quality & Characterisation Standards, alongside presentations by IIT Madras and industry experts.

In his welcome remarks, Prof. M.S. Ramachandra Rao, Head, InCent-LGD, IIT Madras, said, “We have been working on diamond-related research for the last two decades, including projects with industry, space and defence organisations, and that experience led to the Government of India entrusting us with this national centre. Our vision is to develop indigenous technologies and take diamond beyond being just a gem crystal into electronic- and quantum-grade applications.”

In his speech, Sanket Patel, Convener – LGD Committee, GJEPC, noted, “Everybody in this industry requires a research centre like this. We come from a business background and understand diamonds, but to think beyond diamonds, this is the place where industry and research must come together. I would urge the entire industry to support the institute because only together can we move forward.”

Offering an academic perspective, Prof. Manu Santhanam, Dean (Industrial Consultancy & Sponsored Research), IIT Madras, said, “This centre provides a unique opportunity to combine high-end research with deep-tech initiatives and industry collaboration. IIT Madras has a strong entrepreneurship ecosystem and translational research focus, which can help scale technologies and enable the industry to compete with the best globally.”

Delivering a presentation on the New BIS Standard for Lab-Grown Diamond Disclosure, Supreme Kothari, Partner, Economic Laws Practice (ELP), informed, “The objective of the new BIS standard is clarity, not conflict. It recognises that natural diamonds and laboratory-grown diamonds are two separate market categories, and therefore requires clear demarcation in terminology so that consumers are not confused about what they are purchasing.”

“The standard also formally recognises that laboratory-grown diamonds have the same chemical composition, crystal structure and physical properties as natural diamonds. At the same time, it prescribes that only ‘laboratory-grown diamond’ or ‘laboratory-created diamond’ can be used for marketing, creating a benchmark for disclosure practices in the industry.”

“While the standard is not mandatory at present, it carries persuasive value. Regulators, consumer courts and marketplaces may rely on it to determine whether there has been misleading advertisement or unfair trade practice under consumer protection laws.”

“On the trade side, laboratory-grown diamonds currently face reciprocal tariffs in the US, and unlike natural diamonds, they are not included in Annex III for automatic exemption. Industry efforts are therefore focused on securing policy parity and clarity under the evolving trade framework.”

The Indian Institute of Gems & Jewellery (IIGJ), an initiative of GJEPC, signed a Letter of Intent (LoI) with InCent-LGD during VAIRAM at IIT Madras to strengthen India’s laboratory-grown diamond (LGD) education and skill ecosystem. The LoI was signed by Debasish Biswas, CEO, IIGJ, and Prof. M.S. Ramachandra Rao, Head, InCent-LGD, IIT Madras. The collaboration will focus on developing joint certification and diploma programmes in LGD technology, integrating industry-oriented training with research-driven academic inputs.

In addition, a book titled Laboratory Grown Diamond – Production Technologies and its Applications, authored by N. Arunachalam, S. Krishnakanth and T. Mukhilan, was also launched on the occasion.

Key Takeaways — InCent-LGD, IIT Madras Introduction by Prof. M.S. Ramachandra Rao

- India is a major LGD producer but lacks core technology ownership

India is the world’s second-largest producer after China, with thousands of MPCVD machines in Surat, yet indigenous HPHT technology and advanced CVD systems remain limited, creating strategic dependence. - InCent-LGD is focused on indigenous machine development

The centre is developing domestic MPCVD (Vajratara) and HPHT (Vajrakaya) systems with complete process recipes to reduce imports and build national capability. - Beyond gems is the long-term strategic direction

Diamond’s exceptional thermal, electrical and optical properties position it for electronics, quantum devices, photonics, power electronics and advanced industrial applications. - High-quality, defect-controlled material is a core research priority

Work is focused on large-area wafers, controlled defects, high-purity growth and characterisation to enable semiconductor and quantum applications. - India needs a full ecosystem, not just growth capacity

Challenges include lack of seed certification, plasma diagnostics, process control and system selection frameworks, which currently limit yield and efficiency across industry. - AI-enabled smart manufacturing is part of the roadmap

Digital twins, machine learning, plasma monitoring and advanced diagnostics are being integrated into next-generation MPCVD systems to improve consistency and productivity. - Diamond marking technology has been developed for traceability

The centre has created VajrĀnkTM, a proprietary laser marking approach below the top surface for seeds and finished diamonds that enables branding and identification (company logos, designs, QR Codes, etc.) without damaging material quality, supporting traceability, authentication and process optimisation. - India has an opportunity to lead in “Diamondtronics”

The presentation highlights the potential for diamond-based electronics, including GaN-on-diamond (gallium nitride), Si-on-diamond (silicon) and quantum NV-centre technologies, with a call to establish a diamond foundry in India. - Commercial translation and industry access are key objectives

The centre aims to provide seeds, process know-how, consulting and technology transfer support to industry partners to accelerate adoption. - Government backing is enabling long-term research investment

The initiative is supported by the Ministry of Commerce & Industry, recognising LGD as a strategic technology sector with high employment and innovation potential.

Key Takeaways — Panel 1: From Diamond Research to Startup Ecosystem

Moderator: Mr. Bharatwaj Ramakrishnan, Former Industry Leader & Semiconductor & Deep-Tech Advisor

Panellists:

- M.S. Ramachandra Rao, IIT Madras

- Tamaswati Ghosh, IITM Incubation Cell

- Bala Prasad Peddigari, Tata Consultancy Services (TCS)

- Atul Kulkarni, Ionbond: IHI Group

- Ashvani Kumar, Pristine Deeptech Pvt. Ltd.

- Vraj Trivedi, Q2-Maitri Diamonds

- India must shift from manufacturing scale to innovation scale

The LGD sector has strong production capability, but future growth depends on translating research into IP, startups and commercial technologies. - IP should be treated as a monetisation tool, not a trophy

Industry is underutilising intellectual property. Protecting IP early and using it as a currency for collaboration can accelerate commercialisation and partnerships. - Collaboration gaps remain the biggest bottleneck

Weak linkages between academia, industry and end-users are slowing technology adoption. Consortium-based models involving institutes like InCent-LGD, BARC and industry were strongly recommended. - Move beyond the “carat economy” toward a technology economy

Diamonds are increasingly valued for functional properties such as thermal management, electronics and quantum applications, requiring a mindset shift across industry. - Commercialisation barriers are more structural than technical

Technology readiness exists, but challenges include capital intensity, investor expectations, government procurement delays and limited pilot-scale infrastructure. - India has a strategic opportunity to lead in next-gen materials

With large CVD capacity and risk-taking entrepreneurs, India can leapfrog into areas like GaN-diamond and advanced electronics if supported by policy push and coordinated investment. - Investing in startups is critical for ecosystem growth

Industry participation as investors and partners in deep-tech startups is essential to convert research into scalable businesses and global products. - Clear strategic direction: “Invent, Validate, Scale from India”

The panel emphasised moving beyond Make in India toward innovation-led global leadership, with calls to convert “carats into qubits” through technology integration.

Key Takeaways — Panel 2: HPHT Diamond Growth: Technology Evolution & Scale-Up

Moderator: Prof. K. Hariharan, Department of Mechanical Engineering, IIT Madras

Panellists:

- N Arunachalam, IIT Madras

- K.C. Hari Kumar, Department of Metallurgical and Materials

- Engineering, IIT Madras

- Natarajan Ramamoorthy, EGS Computers Pvt. Ltd.

- Manish Jiwani, Anand International

- HPHT remains a complex deep-tech challenge

Generating and sustaining ultra-high pressure (5-6 GPa) and temperatures above 1300°C within the reaction volume, while maintaining equipment integrity and process stability, is a major scientific and engineering hurdle. - Supercell design and catalyst behaviour are critical gaps

Limited understanding of catalyst chemistry, material behaviour under extreme conditions, seed preparation and carbon transport mechanisms continues to constrain yield optimisation and scalability. - Indigenous press development is progressing but needs ecosystem support

India is making advances in prototype HPHT systems and supercell components, but scaling to commercial production requires manufacturing ecosystems, supply chains and industry participation. - Reliability, tolerance and process discipline determine commercial viability

Precision engineering, alignment, durability across cycles and cost efficiency are as important as pressure and temperature parameters in achieving sustainable industrial output. - Strong potential for India to replicate CVD success in HPHT

The panel emphasised that India’s entrepreneurial capability, combined with institutional research and policy support, can enable leadership in HPHT technology similar to its rise in CVD production. - Government-industry-academia collaboration is essential

High capex, uncertain ROI and technology risks require coordinated intervention through policy incentives, funding support and joint development programmes to accelerate adoption. - Applications extend far beyond gems

HPHT diamonds have major opportunities across abrasives, sensors, electronics, radiation detection and semiconductor applications, with demand already significant in industrial segments. - Smart manufacturing and AI integration are emerging priorities

Incorporating sensors, data analytics and predictive control into HPHT systems can reduce failure rates, improve yields and optimise energy and material usage. - India faces strategic urgency due to external dependencies

Reliance on imported HPHT machines and potential geopolitical restrictions underline the need for domestic capability development. - Momentum exists, but coordinated execution is the next step

With research institutions advancing rapidly and industry interest growing, the panel concluded that success now depends on sustained collaboration and investment.

Key Takeaways — Panel 3: Lab-Grown Diamonds Beyond Gems – Opportunities, Challenges and Way Forward

Moderator: Prof. Sathyan S., InCent-LGD, IIT Madras

Panellists:

- Devi Misra, IIa Technologies & IIT Bombay

- Amit Patel, Supreme Green Diamond Pvt. Ltd.

- Amit Banerjee, Microsystem Design-Integration Lab

- Rajaganesh K., InCentLGD, SSMG Group

- Value migration lies beyond substrates toward devices

Moving up the value chain from gem-grade and industrial substrates to functional devices offers significantly higher commercial returns, particularly in electronics, photonics and quantum technologies. - Thermal management and coatings emerge as near-term opportunities

Thermal-grade wafers, heat spreaders, coatings and cutting tools are among the most accessible entry points, leveraging existing CVD infrastructure with moderate process upgrades. - Market creation is as critical as technology development

Even technically viable applications require sustained industry effort to build customer confidence, demonstrate performance and establish commercial demand. - TRL awareness is essential for industry decision-making

Understanding technology readiness levels helps companies assess risk, investment timelines and commercial feasibility when diversifying beyond jewellery applications. - Infrastructure and characterisation gaps are slowing progress

Limited access to advanced testing tools, polishing technologies and post-processing capabilities remains a major constraint for scaling non-gem applications. - Collaboration failures between industry and academia persist

Communication gaps, trust deficits and slow engagement mechanisms are delaying translation from research to commercial products, highlighting the need for structured partnerships. - Corporate labs and consortium models can accelerate innovation

Joint industry-academia facilities, shared infrastructure and coordinated development programmes were identified as effective pathways to bridge the commercialisation gap. - India holds manufacturing scale advantage but must target applications

Existing reactor capacity and process know-how provide a strong base, but success depends on aligning production with specific application requirements rather than generic material output. - Quantum and advanced electronics remain longer-term bets

While sensing applications show promise, large-scale quantum computing and high-end semiconductor integration are still at early development stages globally. - Unified ecosystem action is the central requirement

The panel emphasised joint responsibility across industry, academia and government to convert technical capability into globally competitive products and markets.

Key Takeaways — Panel 4: LGD Quality and Characterisation for Technological Applications

Moderator: Dr. Sairam T N, InCent-LGD, IIT Madras

Panellists:

- Prof Vidya Praveen Ballamudi, IIT Madras

- K.J. Sankaran, CSIR-IMMT, Bhubaneswar

- Tanmay Basu, TCG Crest

- Maneesh Chandran, NIT Calicut

- Nikhil Alfred, IGI

- Technology applications require new grading frameworks

Existing gemological standards are inadequate for deep-tech use cases, creating an urgent need to define electronic-grade, thermal-grade and quantum-grade classification based on material performance and defect levels. - Characterisation is as critical as growth technology

Reliable measurement of defects, impurities, surface functionalisation and crystallographic quality is essential to validate materials for high-tech deployment and commercial adoption. - Diamond properties often exceed equipment limits

Extreme hardness, thermal conductivity and insulating behaviour make characterisation technically difficult, with many standard instruments unable to measure high-quality material accurately. - Advanced infrastructure gaps are slowing progress

Access to high-end tools such as SIMS, high-resolution spectroscopy and specialised thermal measurement systems remains limited, constraining research and industrial translation. - Shared consortium facilities offer the most practical solution

Centralised characterisation hubs supported by industry-academia collaboration are more viable than individual companies investing in expensive equipment with limited utilisation. - Defect engineering enables next-generation applications

Controlled impurities and engineered defects are fundamental for quantum sensing, photonics, electronics and electrochemical technologies, shifting defects from a limitation to a functional asset. - Industrial trust depends on validated benchmarking data

Credible specification sheets, third-party testing and standardised benchmarking are necessary to build confidence between academia and industry and accelerate technology transfer. - Multiple form factors expand application potential

Polycrystalline coatings, nanostructured diamonds, doped electrodes, thin films and bulk single crystals each serve different industrial and technological applications. - Surface engineering and adhesion remain major challenges

Coating adhesion, substrate compatibility, polishing and impurity control continue to limit scalability for mechanical and electronic applications. - Certification and detection technologies are evolving with AI

Machine learning-based detection and fluorescence analysis are improving LGD identification, though rapid process changes by growers create ongoing challenges.

The post VAIRAM 2026 Looks Beyond Gems, Spotlights LGDs’ High Value Deep-Tech Applications appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The post India Can Lead the Next Materials Revolution with Diamonds: IIT Madras appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>VAIRAM 2026 is strongly focused on moving from research to commercialisation. What progress has InCent-LGD made over the past year?

Over the past year, we have made significant progress in several priority areas that were outlined earlier. One notable achievement is the development of diamond marking technology that enables identification without damaging the material quality. This is a first-of-its-kind approach and required substantial research effort.

If you compare what we projected last year with what has been achieved now, the progress has been quite substantial. We are moving steadily toward technologies that are closer to industry adoption.

You have consistently emphasised indigenous capability in CVD and HPHT systems. How close is India to reducing import dependence?

In CVD technology, we are almost there. I would say that within the next six to eight months, we should have our own indigenous CVD machine ready.

For HPHT, we have already developed a prototype. However, a commercial-scale system will take longer, possibly another year to a year and a half. That said, I am confident that India will reach that stage.

Which applications beyond gems are showing the most promise today?

For me, diamond is far beyond gemstones. There are numerous opportunities in electronics, quantum technologies, high-power devices and magnetometry. Diamond is a next-generation material for many of these applications.

The key challenge is achieving extremely high purity levels. Gem applications do not require the same level of purity as electronic applications, where material quality becomes critical. Once that barrier is addressed, the opportunities expand significantly.

Have you seen stronger engagement from manufacturers, start-ups or investors over the past year?

Yes, there is growing interest. Manufacturers are approaching us to understand when the technologies will mature enough for them to invest. I believe that by the end of this year, we will see some technologies transitioning into larger-scale deployment.

The ecosystem is gradually aligning, which is encouraging.

From a policy perspective, what interventions could accelerate India’s leadership in this sector?

Two priorities stand out. First, India should aim to become a global leader in electronic-grade and quantum-grade diamond production. This is where the highest value lies, and it moves us beyond gemstone manufacturing.

Second, we need indigenous certification systems. Currently, we rely heavily on foreign entities for certification. With our capabilities, we should develop standard operating procedures and certification frameworks within India, especially for lab-grown diamonds.

What breakthroughs do you foresee in the near future?

One major focus is developing quantum-grade diamonds with controlled nitrogen-vacancy (NV) centres. Once we achieve that level of control, we can start building devices based on these materials, particularly for magnetometry and nuclear magnetic resonance applications.

These areas have strong potential and could open new technology markets.

You have previously spoken about India missing the silicon opportunity. How can India ensure it does not miss the ‘diamond opportunity’?

The key is perseverance and sustained effort toward clearly defined goals. We must continue investing in research, infrastructure and talent without losing momentum.

From what I see today, we are on track. If we maintain this pace and alignment across academia, industry and policy, I am confident that India will not miss the diamond opportunity.

What would success look like for India in the next few years?

Success would mean India becoming not just a manufacturing hub, but also a technology leader in next-generation diamond applications. That includes indigenous machines, advanced materials, device development and certification capabilities — a complete ecosystem.

The post India Can Lead the Next Materials Revolution with Diamonds: IIT Madras appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

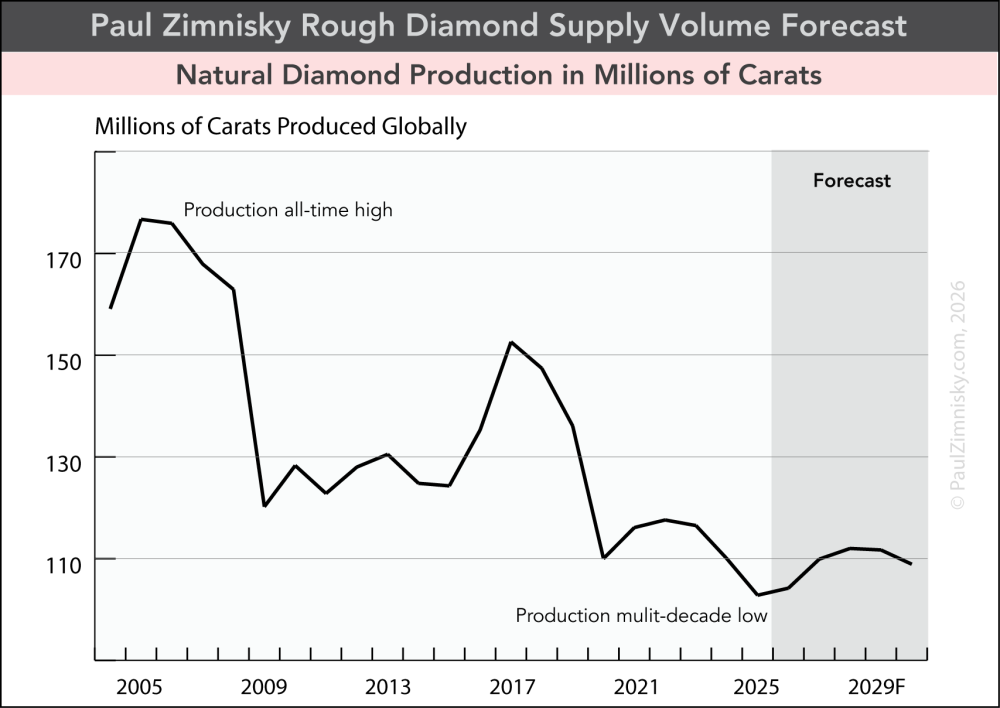

]]>The post Natural Diamond Production to Remain at Multi-decade Lows in 2026 appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>In early-February, De Beers’ parent Anglo American reiterated an approach to “align (diamond) output with prevailing demand” and consequently cut 2026 production guidance to rather wide range of 21 to 26 million carats, down from a previous 26 to 29 million carats.

The move follows a similar adjustment to early last year when Anglo cut De Beers’ 2025 guidance to 20 to 23 million carats, significantly down from the previous range of 30 to 33 million carats.

The latest development is indicative of a natural diamond market that is still jockeying for a recovery following three consecutive years of recession.

Globally, natural diamond supply was estimated at just over 100 million carats last year, according to Paul Zimnisky estimates, marking the lowest annual output since 1992. In 2026, supply is forecast to just moderately rebound to around 105 million carats. For context, this is down from over 150 million as recently as nine years ago (see above figure).

While the current aggressive paring of supply is due in part to legacy mines reaching depletion (production that is not being replaced with new sources), the aforementioned De Beers “supply control” strategy is unequivocally the most poignant factor. It is estimated that De Beers is currently producing at as much as 35% under capacity. Russia’s ALROSA, the world’s largest producer by volume, is also presumably producing at below capacity, albeit at a more moderate 15%, according to Paul Zimnisky estimates.

This mechanism means that as natural diamond demand returns, over 10 million carats of additional production can theoretically be turned back on in relatively short order. Longer term, higher prices could economically drive green- or brownfields development which could take production somewhere around the midpoint of current levels and the highs of 2017.

De Beers and ALROSA currently account for about half of global production by volume (taking into account the curtailed output) with the balance coming from Angola’s Endiama, independent producers and less-commercial alluvial operations, which only represent a single-digit percentage of global supply.

Why almost every other major producer has recently cut supply, Endiama has steadily grown output to over 15 million carats in 2025 – double the level from just five years ago. The company, which is primarily a state-owned entity, operates two of the largest diamond mines in the world: Catoca and Luele. A production ramp-up in the latter has been the primary driver of its supply growth.

Supply by independent producers has notably fallen off in recent years. For example, Petra Diamonds has seen its output fall by some 25% to under 3 million carats relative to five years ago as its two key assets, Cullinan and Finsch, become more difficult and costly to operate with age. Burgundy Diamond’s Ekati mine has seen its production halve to under 3 million carats in recent years as the mine requires costly capex to maintain full operations –conditions which have been squeezed by the softer diamond market.

Finally, Rio Tinto, one of the world’s premier diversified miners, is currently in the process of closing Diavik due to economic depletion – its only remaining producing diamond mine. Daivik produced upwards of 7 million carats annually as recently as 2019.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Paul will be giving a keynote presentation at the Prospectors & Developers Association of Canada (PDAC) Convention in Toronto, Canada on March 2, 2026.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Mining Ltd, a publicly-traded Canadian company with an operating diamond mine in Brazil and a development-stage asset in Angola. None of the above constitutes investment advice, please read full disclosure at www.paulzimnisky.com.

The post Natural Diamond Production to Remain at Multi-decade Lows in 2026 appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The post India-EU FTA Opens Doors, But Design & Quality Will Define Success in Europe: Vivek Shah appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>

Europe is a diverse market with distinct aesthetics and consumer preferences. Based on your 23 years of experience, how can Indian exporters better understand the European buyer’s mindset and design expectations?

The beauty of Europe is that it is like many markets rolled into one with distinct design aesthetics. Northern Europe and Southern Europe is different in terms of aesthetics, and Germany has its own distinct way of purchasing and ordering. Taken together, Europe is an extremely important market for India. Hopefully, with the new trade deal, we will now be able to reach even the interior regions of Europe.

European buyers generally take more time to decide when making deals. They look for extremely high quality, and don’t compromise on any aspect of its aspects—be it settings, gemstones, diamonds, or finishes. Also, their quantities are not huge. They usually buy mixed assortments and are extremely particular about design.

But once they filter out these parameters and select their partners, they genuinely look for long-term relationships.

That is starkly different from the US market, which is unpredictable — a vendor may buy from you today, but move on tomorrow. This is why we enjoy working with European buyers because they value continuity and build business relations that last long.

So, if we want to export to Europe, we must be certain that we can deliver the level of service they expect — especially in design development. We need strong insights, deep product knowledge, and the ability to work at a detailed design level.

Once the FTA is applicable, we will also exploring sourcing certain raw materials such as gemstones, gold chains, locks and clasps from Italy. That, too, can become a huge win-win situation.

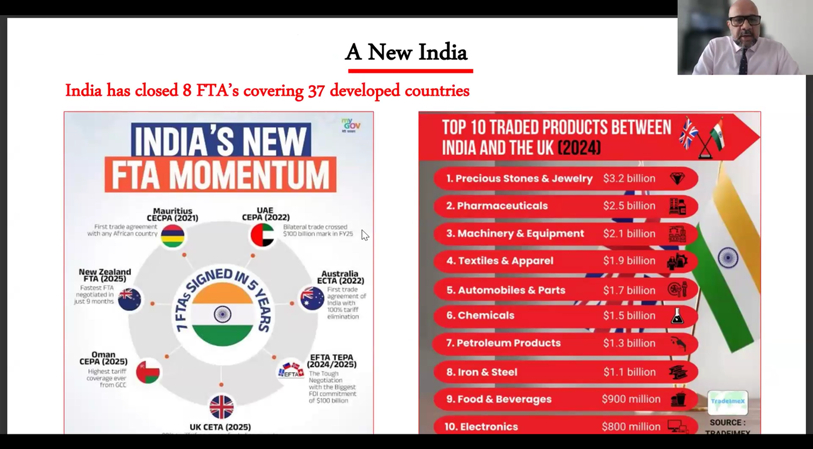

Having exported to European markets for over two decades, how much of an increase in export growth (in percentage terms) do you anticipate following the signing of the EU–India FTA?

We expect an increase 20% to 25% to EU nations in the near future.

What do you see as the key strengths of Indian jewellery exporters today, and how are Indian manufacturers and brands currently perceived by buyers and partners in Europe?

Indian companies go to great lengths when it comes to servicing customers. We genuinely ensure that we don’t let them down – whether it is design development or technical modifications.

Europeans appreciate this approach and they value transparency in dealings.

I believe that is one of the key reasons we have been exporting our high-design sterling silver and gem-studded silver and gold collections to the region for more than two decades, even before this landmark trade deal was signed.

Now our path will be smoother and open more avenues for future growth, thus doubling our current exports to the region in a few years!

Overall, the FTA will push the entire gem and jewellery sector towards higher-end positioning, better quality standards and broader design appeal, while making exports more profitable and sustainable.

The post India-EU FTA Opens Doors, But Design & Quality Will Define Success in Europe: Vivek Shah appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The post Neil Sonawala On Why Natural Diamonds Continue to Shine Through Economic Uncertainty appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>

‘What is scarce is precious’, this adage is turning out to be true of natural diamonds. After being pushed into the corner by the demand for the mass-produced laboratory-grown diamonds (LGDs) for a decade, it is experiencing a renaissance. This has less to do with trends being cyclical and more about the fact that mined diamonds have showcased a remarkable ability to adapt and endure, especially in an era defined by economic uncertainty and rapidly shifting consumer priorities. Despite recent market pressures, natural diamonds held over 71% share of the global market share in 2025.

The rush for natural diamonds is not rooted in nostalgia, but in their evolving relevance to contemporary lifestyles and values. As consumers navigate volatile markets and redefine what luxury means to them, these gems have emerged as timeless treasures that bridge the gap between aspiration and everyday indulgence.

This mindset change can be traced to the diamond market, which is witnessing a fundamental transformation in how and why consumers purchase these precious stones. Traditional milestones like engagements, anniversaries and landmark birthdays, while still significant, no longer singularly define diamond buying. Instead, they now serve as instruments of self-expression and markers of personal achievement. Expressing oneself goes beyond chunks of jewellery, it includes everyday diamond-studded luxury accessories that reflect broader changes in consumer psychology.

A diamond necklace worn daily to the office becomes a reminder of career progress. Stud earrings commemorate a hard-won promotion. A delicate diamond bracelet celebrates self-love rather than waiting for external validation.

Largely emotion-led, this reinterpretation of diamonds has breathed new life into the category. Consumers no longer reserve their finest pieces for rare moments, they integrate diamonds into their daily wardrobes, treating them as wearable confidence boosters and visible symbols of their own journeys of who they are and what they have achieved.

Economic volatility also has a curious effect on consumer behaviour. While spending often contracts during uncertain periods, investment in tangible assets with enduring value tends to rise. Natural diamonds occupy a unique position in this landscape as they are simultaneously emotional purchases having long-term value.

Unlike many consumer goods, including LGDs that depreciate the moment they leave the store, quality natural diamonds retain intrinsic worth. Their rarity is a geological fact, where each stone represents millions of years of the Earth’s processes, creating a scarcity that no technological or scaled manufacturing can replicate. With limited supply projected to lift prices up to 15%, this inherent rarity adds to natural diamond’s value, making them assets that can be worn, enjoyed and eventually passed down or liquidated, depending on the circumstances.

In volatile economic climates, this dual nature becomes particularly compelling. A natural diamond offers psychological comfort and aesthetic pleasure while remaining a portable, durable store of value. It is, quite literally, an investment you can wear. One that does not sit idle in a locker but lives alongside its owner, building emotional and symbolic value over time.

The evolution of diamond jewellery design has played a significant role in reinforcing the relevance of natural diamonds. Contemporary designers have liberated diamonds from the formal rigidity of past generations, reimagining them for modern lifestyles without compromising elegance. Refined craftsmanship now prioritises versatility and ease of wear. Delicate pavé detailing delivers brilliance without excess. Architectural settings allow diamonds to interact with light in unexpected ways. Layer-friendly silhouettes invite personal styling and everyday experimentation. The result is jewellery that moves effortlessly across contexts, from workdays to weekends and from minimalism to fusion.

Today’s consumers want luxury that adapts, not dictates. Natural diamonds, reinterpreted through contemporary design, meet this expectation with ease. It’s open to nuances and thoughtful detailing that come from craftsmanship, appealing to discerning consumers who value distinction.

However, clear documentation, reputable grading and responsible sourcing practices reassure consumers that their purchase aligns with both their values and their expectations of quality.

Equally important is storytelling. By articulating a diamond’s journey, from deep within the Earth to a finely crafted piece of jewellery, brands elevate the purchase beyond transaction.

These narratives reassert why natural diamonds continue to hold emotional and cultural weight in an era dominated by immediacy and abundance.

Trusted brands also act as educators, demystifying diamond value and guiding informed choices. This is necessary to sustain relevance and ensure new generations understand not just how to buy diamonds, but why natural diamonds endure.

The resilience of natural diamonds in today’s economy lies not in resisting change, but in evolving with intention. In uncertain times, people gravitate towards objects that offer beauty, meaning and permanence. Natural diamonds continue to deliver all three quietly, confidently and permanently.

The post Neil Sonawala On Why Natural Diamonds Continue to Shine Through Economic Uncertainty appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>The post Suvankar Sen: “From Lightweight Lines to Old Gold Exchange, We’re Redefining Demand” appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>With gold prices staying elevated, how is Senco recalibrating product mix and price points to keep demand steady without diluting margins?

Elevated gold prices are not reducing consumer’s intent; they are reshaping how consumers enter the category. Our strategy at Senco Gold & Diamonds has therefore been structural, not promotional. Instead of relying on discounting, we are strengthening design-led, lightweight collections that reduce gold weight per piece while preserving visual appeal and craftsmanship value.

Collections such as Everlite, available across 9-, 14- and 18-karat gold, offer more accessible ticket sizes and cater to modern daily-wear needs. At the same time, we are increasing the share of diamond jewellery and solitaire-led ranges like Perfect Love, where the value proposition is driven more by design and gemstone than metal weight.

Operationally, the focus is on design efficiency, carat optimisation, and higher design value per gram. Exchange-driven upgrades and structured purchase pathways further help customers manage budgets without compromising margins. The result is demand continuity supported by smarter product architecture rather than price intervention.

What safeguards are required in regulated small-ticket EMIs to balance affordability with consumer protection and financial discipline?

Small-ticket EMIs can make jewellery purchases more structured and accessible, but the framework must prioritise transparency and responsible lending. Jewellery is an emotional purchase, yet financing must remain rational.

Consumers should receive clear, simplified disclosure of the total cost of credit including interest, processing fees and repayment obligations. Tenures for small-ticket lifestyle purchases should be reasonably capped to avoid long repayment cycles that can lead to debt stress.

Equally important are responsible, credit checks, especially for first-time borrowers, to prevent over-leveraging. Customers should have flexibility through cooling-off periods and easy prepayment options without heavy penalties. Integration with regulated banks and NBFCs, rather than informal credit channels, is essential to ensure compliance and consumer protection. The objective is to support planned affordability, not impulse-led borrowing.

How could a review of the 3% GST practically influence buying behaviour, especially in entry-level and wedding jewellery?

Jewellery purchases are both emotionally significant and value-sensitive, which means even small tax adjustments can have a visible behavioural impact.

In entry-level and lightweight segments, a lower effective tax burden can meaningfully improve affordability and encourage first-time buyers to choose organised retail over informal channels. For wedding jewellery, where ticket sizes are larger, tax rationalisation reduces the overall bill value and can ease the need to defer purchases or rely excessively on old gold exchange to manage budgets.

A calibrated GST review would not simply act as a price lever; it would also strengthen formalisation, improve billing transparency and support organised retail competitiveness, benefiting the broader ecosystem.

What are the key on-ground challenges jewellers face in scaling old gold exchange programs, which now form around 45% of transactions?

Old gold exchange has become a structural driver of the jewellery market, but scaling it involves operational complexity.

The first challenge is purity assessment and customer trust. Even with modern testing technologies, customers often have emotional attachment to legacy jewellery and can be sensitive to melting outcomes and valuation differences. Older jewellery also varies widely in composition and craftsmanship, creating standardisation challenges across regions.

At the store level, exchange transactions are time-intensive, particularly during peak seasons, affecting throughput. There are also documentation and compliance requirements as traceability norms strengthen. From a backend perspective, exchange-led buying changes inventory dynamics, requiring careful balance between recycled gold and fresh procurement.

Successful scaling depends on trained staff, transparent communication, and strong refining partnerships to ensure consistency and consumer confidence.

How can gold exchange help reduce import dependence and improve circulation within the domestic supply chain?

India holds a substantial stock of gold in household form. When this gold re-enters the market through organised exchange programs, it becomes a secondary domestic source of raw material.

Recycled gold feeds local refining and manufacturing, strengthening the internal supply chain, and improving metal circulation within the formal ecosystem. As exchange-led transactions grow, the need for incremental fresh imports at the margin can ease particularly during high-price periods when consumers prefer upgrading existing holdings.

Over time, a robust exchange and recycling ecosystem supports a more sustainable, circular gold economy, helping balance demand and supply in a price-sensitive market like India.

What level of import duty would meaningfully improve competitiveness without significantly impacting revenue?

The import duty calibration is about balance. The objective should be to narrow the gap between official imports and unofficial channels without creating fiscal instability.

A moderate, stable duty structure can improve compliance, reduce grey-market incentives, and strengthen organised retail competitiveness. When duties are perceived as reasonable and predictable, formal trade volumes tend to rise, which can partially offset lower rates through better documentation and wider tax compliance.

Stability and predictability are as important as the rate itself. Jewellers need visibility for pricing and inventory planning, while policymakers must balance competitiveness with revenue considerations. The right calibration encourages legal trade flows and strengthens the formal value chain.

The post Suvankar Sen: “From Lightweight Lines to Old Gold Exchange, We’re Redefining Demand” appeared first on Solitaire magazine is a International jewellery magazine - India’s leading B2B gem and jewellery magazine.

]]>